.avif)

This is the first post in our multi-part series that deep dives into the world of NeSL and Information Utilities.

The importance of debt

A significant chunk of economic activity in any economy is driven by loan debt. Banks and NBFCs disburse loans as financial debt. But what happens when a borrower is unable to pay debts back to a Bank or NBFC? That’s where the Insolvency System kicks in.

The Importance of a Good Insolvency System

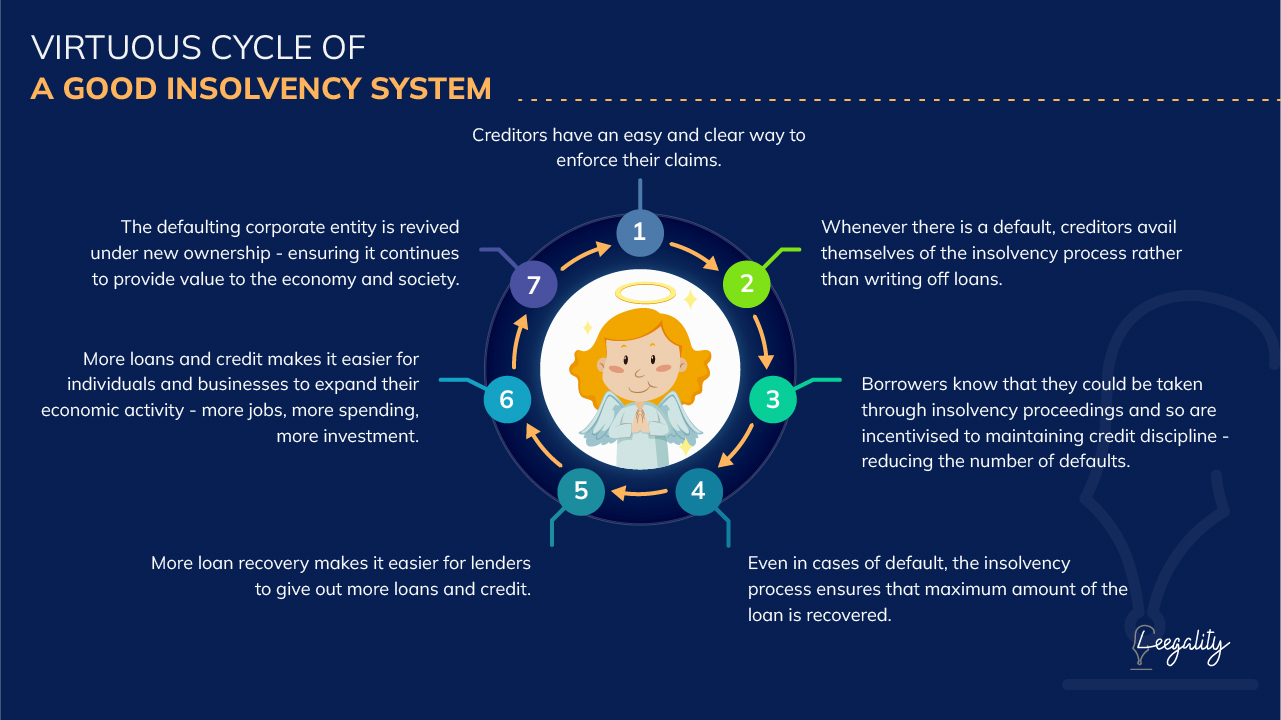

As per the IMF, a good insolvency system - helps enhance the flow of credit, creates credit discipline and provides a way for the economy to “preserve value” from defaulting/sick companies.

The problem with Indian insolvency pre-IBC

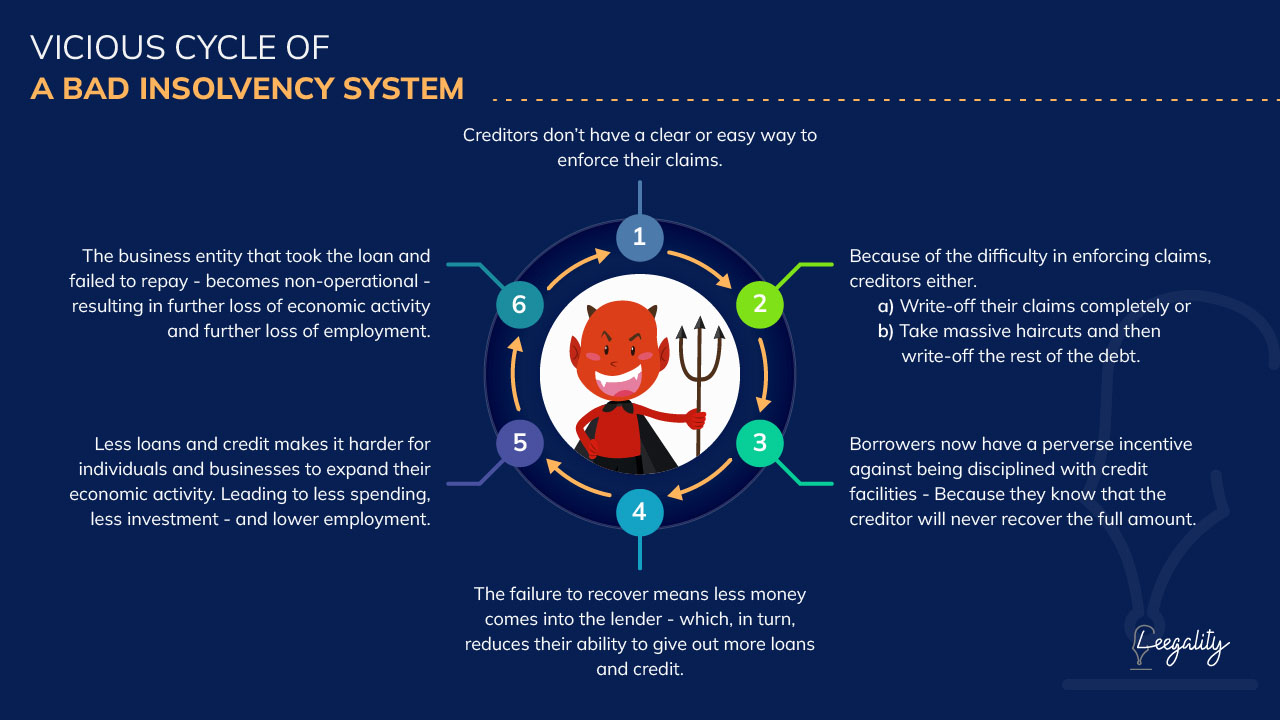

Before 2016, the Indian insolvency system was, to put it very mildly - NOT GREAT. It had three critical problems: it was slow, had low success rates for creditors, and lacked proper process to revive defaulting corporate entities.

The Information Problem with IBC evidence

Conventional modes of creating debt documentation and maintaining debt information create problems that cast evidentiary doubt about their veracity. Borrowers exploit these vulnerabilities to frustrate creditors’ claims - not necessarily to avoid admission, but to protract and prolong the insolvency petition.

A 2021 report by IBBI stated that the insolvency process in India takes an average of 459 days - about 280 days more than the stipulated 180 day time limit in the IBC.

That’s where Information Utilities step in.

----------------------------------------------------------------------------------------------------------------------------

Want to know how exactly Information Utilities solve the Information Problem? Check out our next post.