Gold loan regulation in India used to be scattered across 31 different circulars, issued over decades, for different types of lenders, often contradicting each other.

If you were a compliance head at a gold lending NBFC, figuring out what documentation you actually needed meant piecing together guidance from 31 different circulars issued over several decades.

That changed in November 2025.

The RBI released two Responsible Business Conduct Directions — one for Commercial Banks and one for NBFCs — that replace the entire scattered rulebook.

These are now the master regulations for gold lending in India.

The deadline to comply with these rules has already passed. It was April 1, 2026.

Applicable to: all commercial banks and all NBFCs (including HFCs) lending against gold or silver collateral.

Scope of this blog

This blog covers only the paperwork and documentation rules of the Directions — 6 specific requirements that govern your gold loan agreements, valuation certificates, KFS, and borrower communications.

We are not covering LTV ratios, auction norms, collateral storage, or end-use monitoring. Those are separate topics.

Aim of the RBI gold loan rules

With these Directions, the RBI has prioritized two things: fraud prevention and customer transparency.

The RBI wants a transparent, auditable paper trail for every gold loan, and it expects lenders to build systems that deliver this.

The 6 rules at a glance

Here's a summary of the 6 rules and how to comply:

Rule 1: Standardised documentation across all branches

"Documentation shall be standardised across all branches of the bank."

Clause 368, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025 Clause 48, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025

What the rule means

You have to standardize your gold loan agreement, KFS, sanction letter, DPN, and all other loan documentation.

How to comply

To comply, you have to ensure 3 things:

- Create an agreement kit centrally. All documents, agreements, KFS, valuation certificates, and T&Cs must be drafted, vetted, and finalised by your legal/compliance team at the central level.

- Allow no branch-level editing. Branch staff must not be able to change the content, wording, or structure of any document. The agreement a borrower signs in Coimbatore must be identical in substance to one signed in Ludhiana. Branch staff can fill in transaction-specific facts (borrower name, loan amount, etc). Nothing else.

- Instant version control. When legal/compliance updates a document at the central level — say, adding a new clause because of a regulatory change — every branch must use the new version immediately. No branch should be operating on an old copy.

Rule 2: Mandatory fields in every gold loan agreement

"The loan agreement shall cover the description of the eligible collateral taken as security, value of such collateral, details of auction procedure and the circumstances leading to the auction of the eligible collateral, the notice period which shall be allowed to the borrower for repayment or settlement of loan before the auction is conducted, timelines for release of pledged eligible collateral upon full repayment or settlement of loan, refund of surplus, if any, from the auction of the pledged eligible collateral and other necessary details."

Clause 369, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025 Clause 49, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025

What the rule means

The gold loan agreement must include mandatory details like:

- Description of the collateral

- Value of the collateral

- Auction procedure details

- Circumstances that trigger auction

- Notice period for repayment before auction

- Timelines for collateral release after full repayment

- Surplus refund from auction

- All applicable charges (including assaying and auction charges)

How to comply

You have to ensure that the filled agreement goes to the borrower for eSign. Two ways to do this:

Option 1: Automated filling of mandatory fields

This works if you have an API flow between your LOS/LMS and document execution software.

- If the PDF is generated at the LOS/LMS stage: Your LOS/CBS collects the data, auto-fills the agreement, and generates a PDF, then passes it to the document execution system. The LOS/LMS should block the process if any mandatory field is empty.

- If the PDF is generated at the document execution platform: The platform ensures all mandatory fields are filled before the document goes to the borrower.

Option 2: Manual filling with a checker

If you don't have an API flow between LOS/LMS and the document execution software:

- Branch staff fill in the agreement and send it to a reviewer

- The reviewer checks if all fields are filled and approves

- Only after approval does the agreement go to the borrower for signing

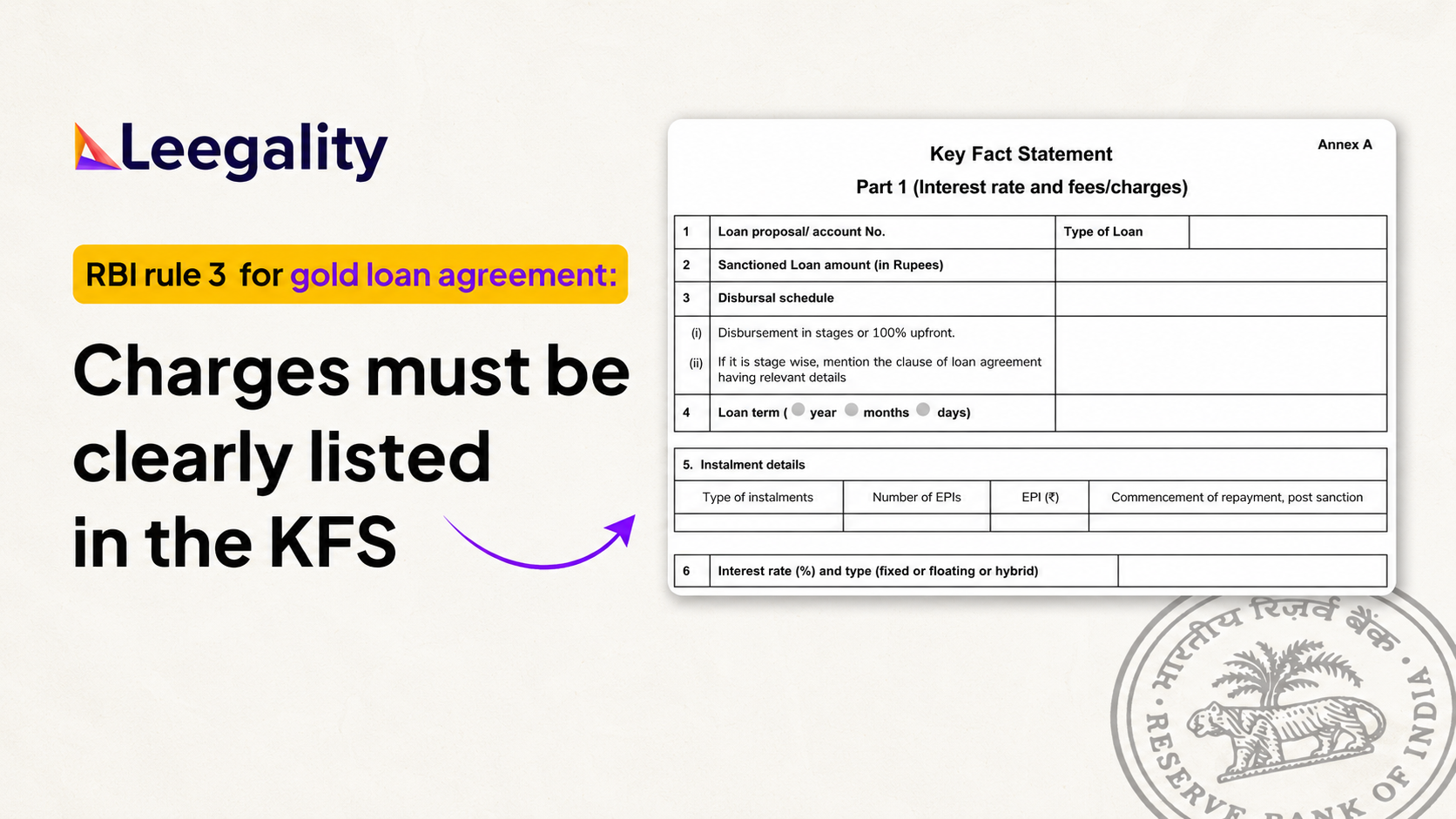

Rule 3: All charges must be listed in the KFS

"All applicable charges payable by the borrower, including those related to assaying, auction, etc., shall be clearly included in the loan agreement and KFS."

Clause 369, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025

Clause 49, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025

What the rule means

This one is fairly self-explanatory. You have to ensure that a filled KFS, with all charges disclosed, goes to the borrower.

You also have to use the RBI-prescribed format: Annexure A, APR computation sheet, and amortisation schedule.

How to comply

Comply with the RBI's 7 KFS operational requirements. See this detailed video for RBI KFS rules and how to comply here.

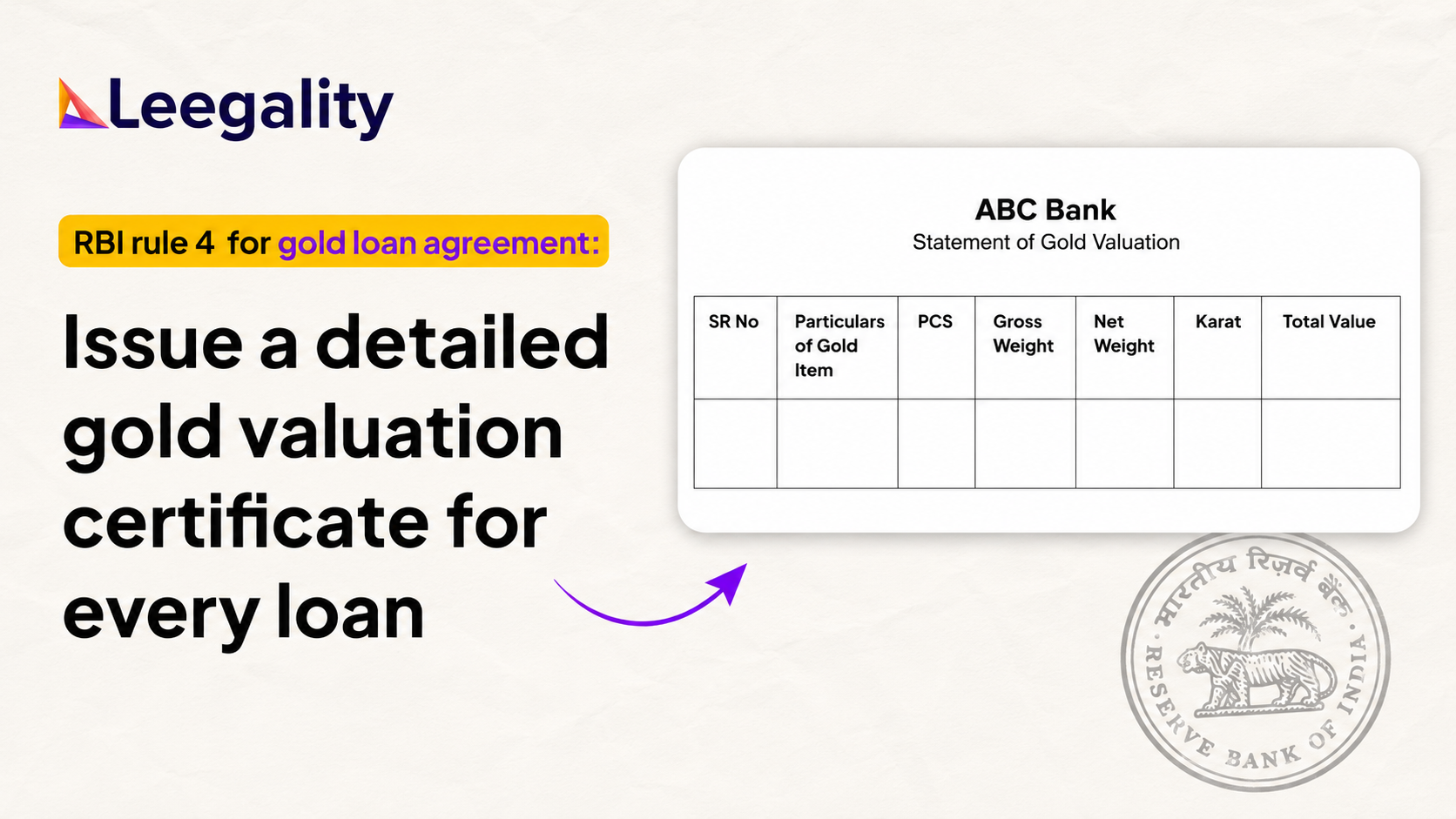

Rule 4: Detailed gold valuation certificate for every loan

"A bank, while accepting the eligible collateral, shall prepare a certificate or e-certificate in duplicate on its letterhead regarding the assay of the collateral and state therein the purity (in terms of carats); gross weight of the eligible collateral pledged; net weight of gold or silver content therein and deductions, if any, relating to weight of stones, lac, alloy, strings, fastenings, etc.; damage, breakage or defects, if any, noticed in the collateral; image of the collateral; and the value of collateral arrived at the time of sanction. One copy of the certificate or e-certificate shall be kept as part of the loan documents and the other copy be given to the borrower under their acknowledgement."

Clause 370, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025 Clause 50, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025.

This is the most operationally demanding of the 6 rules.

What the rule means

You have to ensure that these details are filled before the borrower gets the valuation certificate:

- Purity (in carats)

- Gross weight of the collateral

- Net weight of gold/silver content, with deductions for stones, lac, alloy, fastenings, etc.

- Damage, breakage, or defects (if any)

- Image of the collateral

- Value of collateral at the time of sanction

How to comply

To comply, you have to do 2 things:

- Create the certificate with every mandatory detail. Ensure your LOS/LMS creates the filled valuation certificate — or passes the mandatory field data to the document execution platform, which creates it.

Note: The image of the collateral is now mandatory. If your branches don't already photograph the gold, you need to add this step.

- Send one copy to the customer, keep one copy attached to the loan agreement. The copy to the borrower should go automatically (via WhatsApp, SMS, or email). The copy for your records should auto-attach to the loan file in your LOS/CBS.

We did a detailed video on how to build an RBI-compliant gold valuation certificate process — watch it here

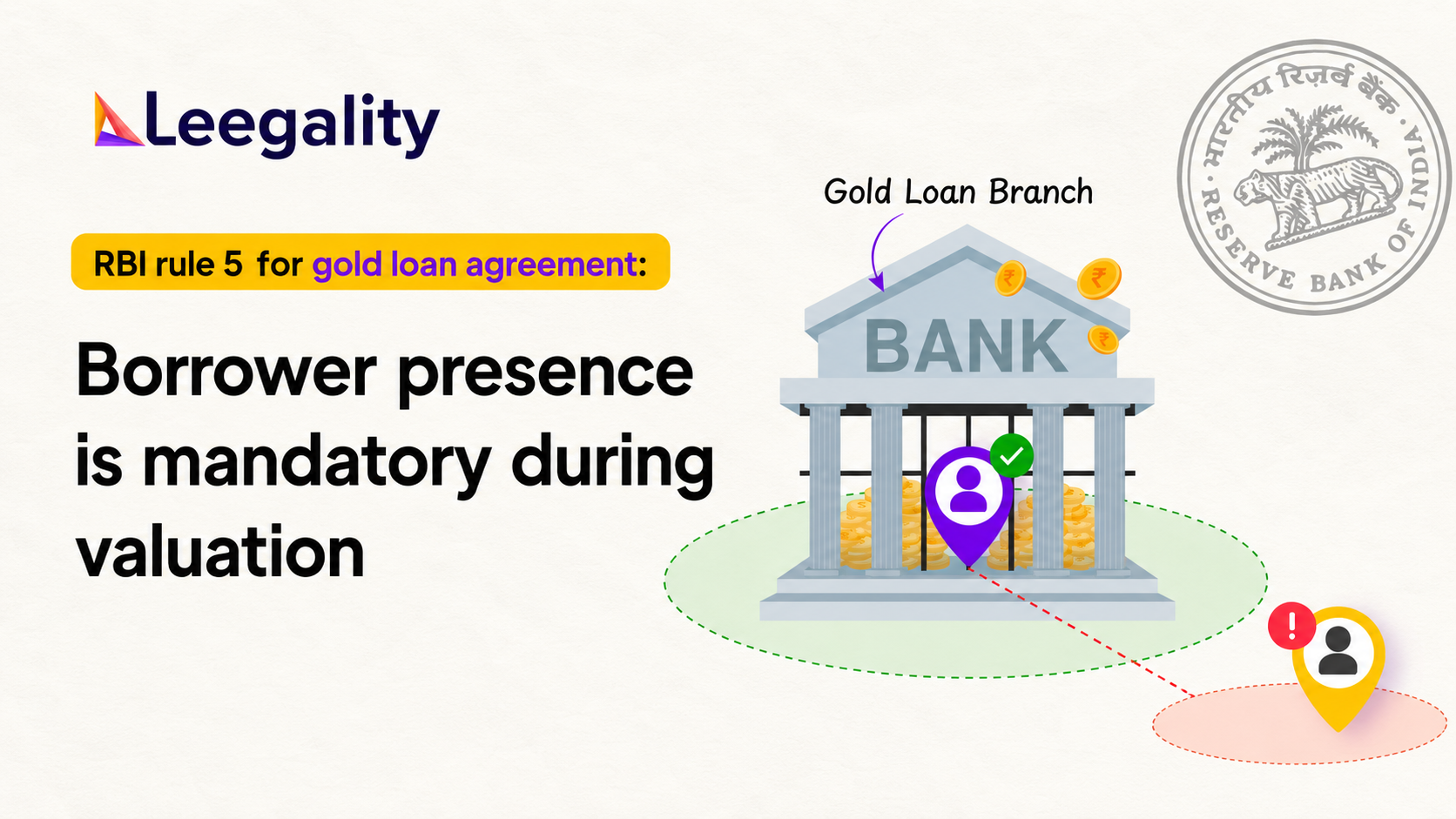

Rule 5: Borrower must be present during valuation

"A bank shall ensure the presence of the borrower(s) while assaying the collateral at the time of sanctioning the loan."

Clause 366, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025 Clause 46, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025

What the rule means

To comply, you have to ensure two things:

- Borrower presence during the valuation of every gold loan and ensure that the valuation can't proceed without the borrower being there.

- Prove borrower presence during RBI audits.

How to comply

Get the valuation certificate eSigned by both the borrower and the valuator — and geofence their location to the bank branch. The eSign can't begin until both are present at the branch.

The Directions require that key terms be explained in front of a witness who is not an employee of the lender. This means:

- Aadhaar biometric signing — an illiterate borrower cannot be expected to use OTP

- Independent witness signature — captured along with their identity (face capture or GPS) for audit purposes

This needs a separate workflow — distinct from the standard borrower flow.

This does two things:

- Prevents the process from completing when the borrower is absent

- Creates a GPS-stamped audit trail showing both parties were at the same location

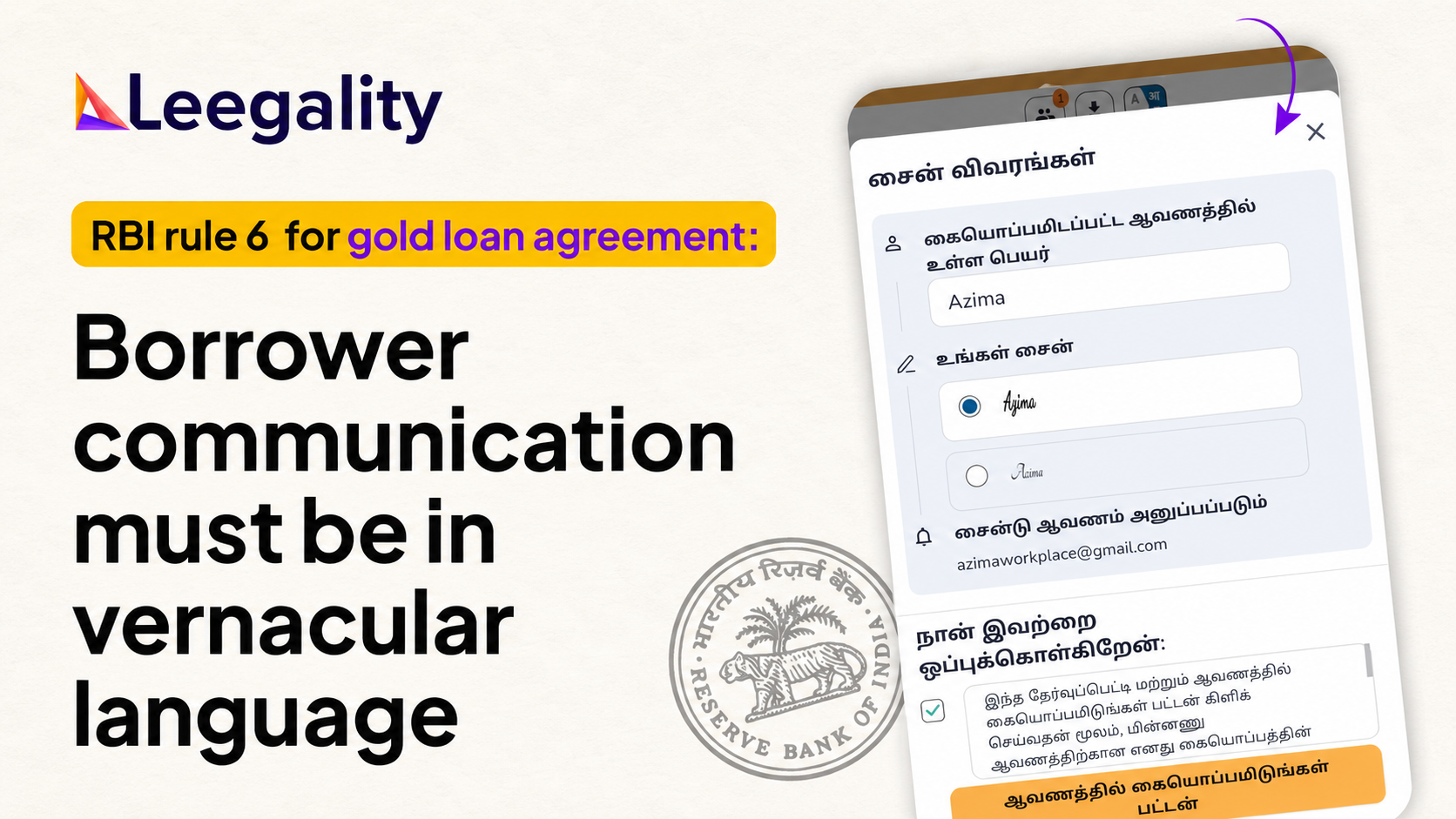

Rule 6: Borrower communication must be in their language

"All communication with the borrower, especially, the terms and conditions of the loan, or other important communication which affects the interest of the borrower or the bank, shall be in the language of the region or in a language as chosen by the borrower. For an illiterate borrower, important terms and conditions shall be explained in the presence of a witness, who shall not be an employee of the bank. "

Clause 371, RBI (Commercial Banks – Responsible Business Conduct) Directions, 2025 and Clause 51, RBI (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025

What the rule means

If your borrower is literate: Your entire gold loan kit — agreement, KFS, valuation certificate, T&Cs — must be available in each language your borrowers need. The specific languages depend on where your branches operate.

If your borrower is illiterate, ensure a witness is present while explaining terms and conditions to the borrower.

How to comply

Show a language selection screen to the borrower, like at an ATM, and allow them to select the language they are comfortable with.

Then execute the eSign journey and the entire agreement kit in that selected language. Watch our detailed product demo of this flow.

.avif)